Automating Capital Management

If you google terms like “AI takes jobs” or “robots replace humans” you find a plethora of contradictory articles. Every writer and their…

If you google terms like “AI takes jobs” or “robots replace humans” you find a plethora of contradictory articles. Every writer and their mother believes they know which jobs will be replaced and which will be safe from the ‘unstoppable tide of automation’. This infinite squabble over the capacity of artificial intelligence seems a bit circular. Rather than shed my own opinion on this debate, I decided to simply examine an industry I have been particularly close to this past few months- retail investors in capital management- and the possible disruption to come.

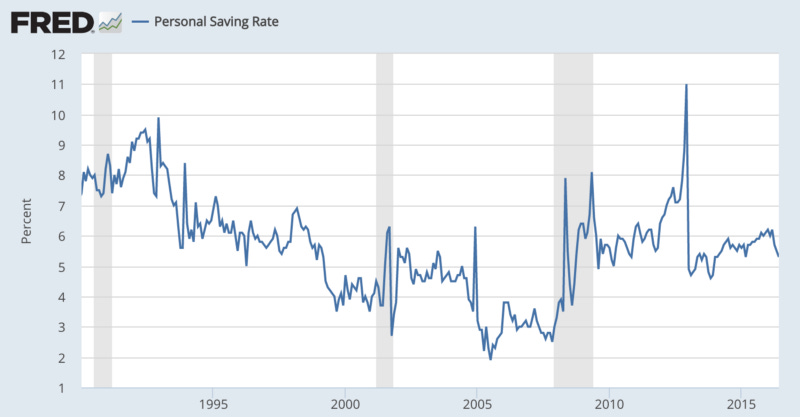

Personal Savings Rate

The rate of savings is relatively low in 2016. After reaching all-time lows in 2005 at about 1.9% and rebounding upwards post-08, we have seen that consumers are only saving 5% as a percentage of personal disposable income. That’s a relatively small deposit compared to just a few years ago, when consumer confidence was lower. This makes sense. Given that interest rates are minimal, investments in the markets may seem a bit more enticing.

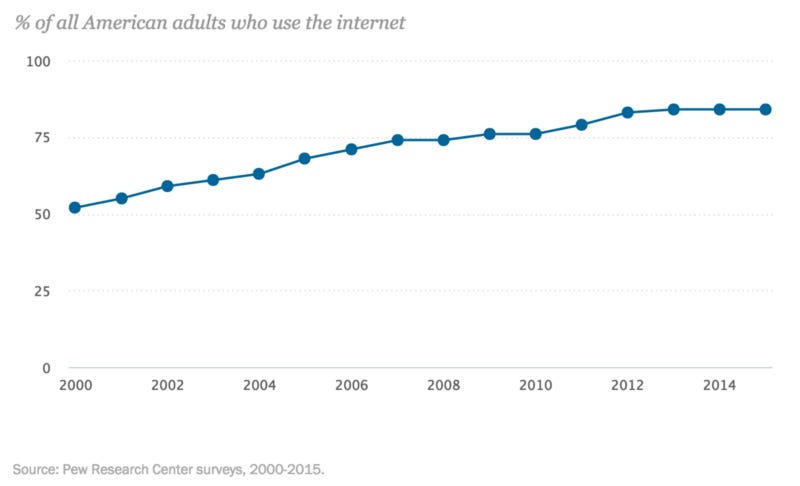

Internet adoption amongst older adults and seniors

More than 99% of teenagers use the internet. While that’s great, it doesn’t mean much in the world of wealth management. Older adults and senior citizens hold most of society’s money. It may seem trivial to consider internet adoption rates, but the technology has been slow to proliferate among older audiences, especially in America. A lack of comfort with internet use indicates an even stronger lack of comfort with investing through online portals.

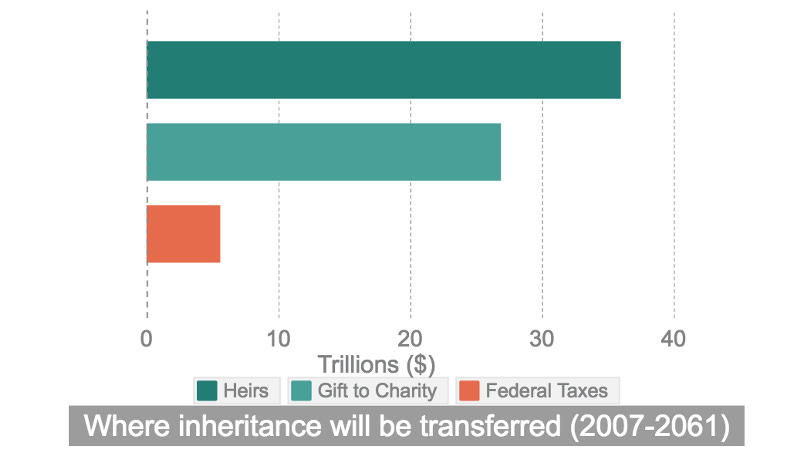

The biggest sum of inheritance we have ever seen

This is a graph from the Boston College Center of Wealth and Philanthropy. It’s expected that more than $35 trillion will transferred to the modest piggy-banks of younger generations within the next 50 years. This is a generation that is more comfortable with operating online and has a far greater faith in robo-advising platforms.

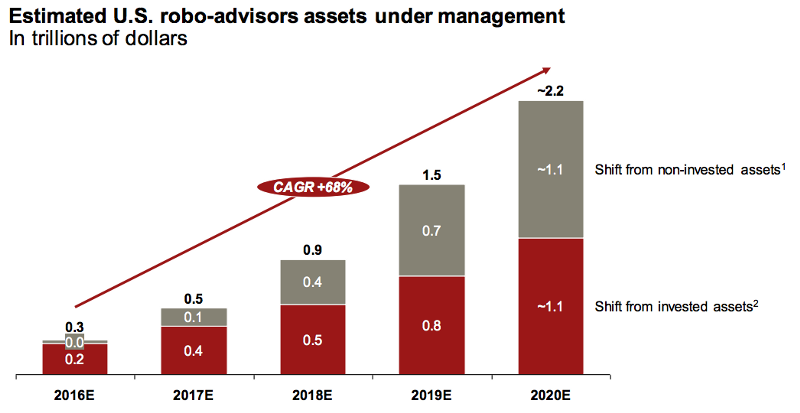

And finally: the tide (or gentle stream) of the robo-advisor:

Large incumbent wealth managers are challenged by the growth of Betterment and Wealthfront. In the face of this disruption they have taken a proactive approach to developing proprietary auto-rebalancing and advising platforms. Consumers across all asset classes are receptive to the option of robo-advisors. More than 48% would consider investing through an automated platform. Since January 2015, Betterment has more than doubled the size of assets under management and opened 40,000 more accounts. From it’s inception in 2011, the Wealthfront platform was able to raise more than $2 Billion in AUM. Each month, thousands more are placing their funds in the hands of these automated platforms.

It seems that robo-advising is inevitable. This does not mean the end for dominant funds, given that they are already beginning to compete with their own platforms. The larger implications are for the thousands of educated, investment professionals whose jobs are now becoming automated. While we have seen, and will continue to see, automation take over jobs that require minimal education, this may be one of the first ‘white collar’ positions that is enormously impacted.

Truly addressing the impact of robo-advising

To really understand the impact that these platforms can have, requires a few steps.

Consider the total market size for investments while keeping in mind changing customer preferences and trends.

Accounting for the limitations robo-advisors will experience while scaling

Estimating total revenue impact on the financial industry

What we have done here is to simply glimpse at some of the factors that contribute towards step one. To finalize an opinion would mean addressing all three considerations.